Page 163 - EM - EXPORT MAGAZINE PERFUMERY EDITION

P. 163

R E P O R T

buyers. Furthermore, the share of

premium class travellers (premium

economy, business and first class

included) among visitors has risen

significantly. This shift points to a more

affluent and discerning customer base,

according to m1nd-set. European

travellers are increasingly prioritising

the in-store experience over price

as a motivator for visiting Travel

Retail shops, the research reveals.

Store attractiveness has grown as a

visit driver, rising from 22% in 2022

to 28% in 2025, while the appeal of

price and promotions has declined.

The research demonstrates that in-

store experience has now emerged

as the number one purchase driver,

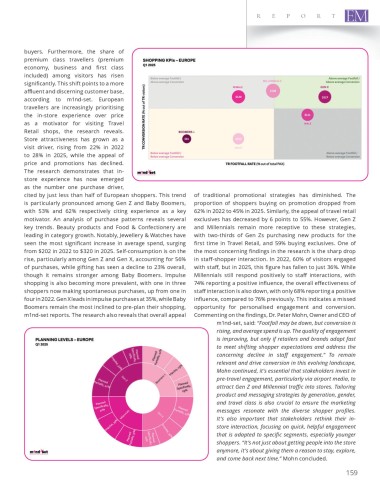

cited by just less than half of European shoppers. This trend of traditional promotional strategies has diminished. The

is particularly pronounced among Gen Z and Baby Boomers, proportion of shoppers buying on promotion dropped from

with 53% and 62% respectively citing experience as a key 62% in 2022 to 45% in 2025. Similarly, the appeal of travel retail

motivator. An analysis of purchase patterns reveals several exclusives has decreased by 6 points to 55%. However, Gen Z

key trends. Beauty products and Food & Confectionery are and Millennials remain more receptive to these strategies,

leading in category growth. Notably, Jewellery & Watches have with two-thirds of Gen Zs purchasing new products for the

seen the most significant increase in average spend, surging first time in Travel Retail, and 59% buying exclusives. One of

from $202 in 2022 to $320 in 2025. Self-consumption is on the the most concerning findings in the research is the sharp drop

rise, particularly among Gen Z and Gen X, accounting for 56% in staff-shopper interaction. In 2022, 60% of visitors engaged

of purchases, while gifting has seen a decline to 23% overall, with staff, but in 2025, this figure has fallen to just 36%. While

though it remains stronger among Baby Boomers. Impulse Millennials still respond positively to staff interactions, with

shopping is also becoming more prevalent, with one in three 74% reporting a positive influence, the overall effectiveness of

shoppers now making spontaneous purchases, up from one in staff interaction is also down, with only 68% reporting a positive

four in 2022. Gen X leads in impulse purchases at 35%, while Baby influence, compared to 76% previously. This indicates a missed

Boomers remain the most inclined to pre-plan their shopping, opportunity for personalised engagement and conversion.

m1nd-set reports. The research also reveals that overall appeal Commenting on the findings, Dr. Peter Mohn, Owner and CEO of

m1nd-set, said: “Footfall may be down, but conversion is

rising, and average spend is up. The quality of engagement

is improving, but only if retailers and brands adapt fast

to meet shifting shopper expectations and address the

concerning decline in staff engagement.” To remain

relevant and drive conversion in this evolving landscape,

Mohn continued, it’s essential that stakeholders invest in

pre-travel engagement, particularly via airport media, to

attract Gen Z and Millennial traffic into stores. Tailoring

product and messaging strategies by generation, gender,

and travel class is also crucial to ensure the marketing

messages resonate with the diverse shopper profiles.

It’s also important that stakeholders rethink their in-

store interaction, focusing on quick, helpful engagement

that is adapted to specific segments, especially younger

shoppers. “It’s not just about getting people into the store

anymore, it’s about giving them a reason to stay, explore,

and come back next time.” Mohn concluded.

159